After the release of the tax reform legislation from the House, last week’s question was "who will be affected by the new bill?"

One of the key elements of the tax reform is the proposed capping of the mortgage interest deduction at $500K. Under the current tax framework, taxpayers who own a home are able to reduce their taxable income by the amount of interest paid on the loan, which is secured by their principal residence. Interest is deductible on only the first $1 million of debt used for acquiring, constructing, or substantially improving the residence ($500,000 for single individuals if filing separately), or the first $100,000 of home equity debt regardless of the purpose or use of the loan. The new tax reform legislation allows homeowners to take the deduction on their first $500,000 of mortgage debt, half of the current threshold. The new threshold will affect only mortgages on purchases made after the law is in force (but will not include refinancing). Thus, a new homebuyer will be able to deduct from his taxable income up to $15,4751 under the new proposed tax framework, while he could deduct up to $30,950 under the current tax framework. Although $500K seems to be a decent amount of money, is it enough to buy a home in all areas in the United States?

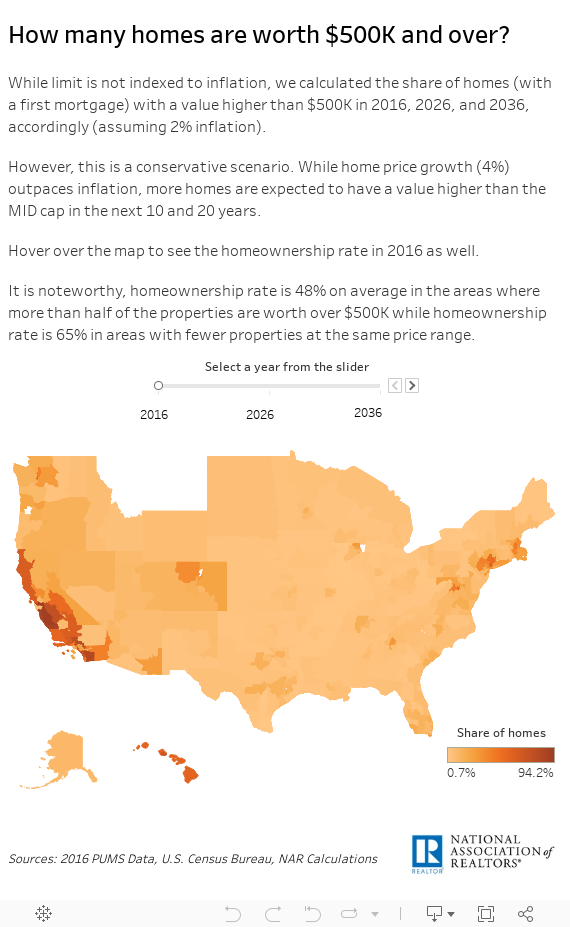

Since all real estate is local, we calculated the share of homes2 with a value higher than $500K by Congressional District. Based on the data, on average, 15% of homes with a first mortgage are worth over half a million dollars across the congressional districts. The share varies from 0.1% (13th District, Ohio) to 94% (14th District, California). Actually, one out of every two homes is worth over half a million in several districts in the following states: California, Connecticut, District of Columbia, Hawaii, Massachusetts, New York, Virginia and Washington.

Furthermore, we should bear in mind that the limit of $500K is not indexed to inflation, causing its value to diminish even further over time. Thus, we took our analysis one step further and calculated the share of homes with a value higher than $500K (subject to an inflation rate of 2%) in 2026 and 2036.

The map below allows you to see the share of homes with a first mortgage and value higher than $500K in 2016, 2026 and 2036.

It is true that the statistics above include people with a mortgage who already own a house. As we already mentioned, the MID cap will be applied to new mortgages only. Thus, someone would argue that these people will not be affected. It is true that there will not be a direct effect on these owners, but we expect that they will be less willing to sell their home. Consequently, homeowners are expected to be less mobile. Finally, the diminished role of mortgage interest deduction will impact home values negatively. By how much is debatable, but all homeowners can expect to lose some portion of their housing equity if the proposed tax bill become the law.

1 In the first year of a 30-year mortgage (assuming a 20% down payment and 3.9% mortgage rate)

2 Only homes with a first mortgage are included