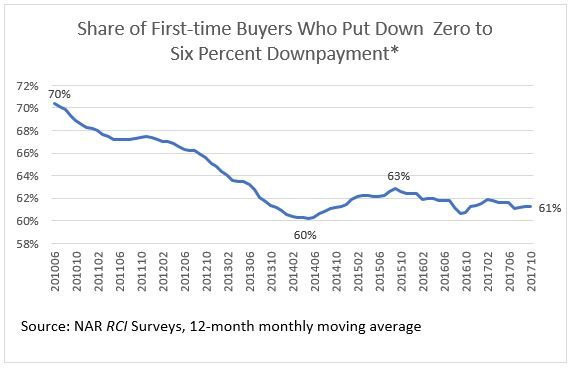

Among first-time buyers who purchased a property through a mortgage in December 2016–November 2017, 61 percent, on average, made a zero to six percent downpayment, according to the November 2017 REALTORS® Confidence Index Survey. The share of first-time buyers who made a zero to six percent downpayment decreased from an average of 70 percent in the 12 months ended June 2010, to a low of 60 percent in mid-2014, then rose in 2014‒2015 to 63 percent, but the share appears to have slightly edged down in 2016 and 2017.[1]

In December 2015, Fannie Mae and Freddie Mac started accepting mortgage applications with as little as three percent downpayment to ease the access to credit for first-time buyers. So why has the share of first-time buyers who obtained low downpayment mortgages not budged up significantly even with these low downpayment conventional financing programs? One reason may be related to the trade-off between a lower downpayment and monthly outlays: a lower downpayment means lower upfront cash outlay, but this also means making higher monthly payments because of the higher interest payments and mortgage insurance premiums.[2]

The author’s calculations show that a 25-34-year-old headed household with median household income of $60,932 in 2016 who intends to purchase a $187,040 property[3] with a 3.5 percent or 5 percent downpayment will pay about $1,500 for principal, interests, taxes, mortgage insurance, and maintenance (PITIM) or nearly 30 percent of income on housing cost, a threshold for cost-burdened households. With a 20 percent downpayment, the monthly PITIM declines to $1,138, or 23 percent of income, because of lower interest payments and zero payments for mortgage insurance, making the mortgage more affordable.

On the other hand, the downpayment sharply increases from $6,546 to $37,408. The 20 percent downpayment will be hard to meet, given that the average savings of non-homeowners was only $5,200 in 2016, according to the Federal Reserve Board’s 2016 Survey of Consumer Finances.

Thus, making a home purchase more affordable will require either a deceleration in price growth, an acceleration in income growth, or expanding downpayment assistance programs so to help buyers make a higher downpayment and lower monthly costs.

Household income has grown at a modest pace, rising by about 20 percent since 2012, while home prices have increased by roughly 60 percent. A deceleration in home price appreciation will largely come if supply increases to meet household formation and replacement for housing demolitions or destroyed housing, which NAR Chief Economist Lawrence Yun estimates to be at 1.5 million units. Housing starts have more than doubled to an annual pace of 1.29 million units as of October 2017 (from a low of 490 thousand in January 2009), but the pace has not been adequate to meet housing demand, as evidenced by the steep price growth.

Downpayment assistance programs are another way to make a home purchase more affordable. One mechanism is through state-funded downpayment savings accounts, with states allowing contributions to and/or the interest earned on these accounts to be income tax deductible[4]. Currently, Iowa, Minnesota and Mississippi, Colorado, Montana and Virginia provide implement these programs. Alabama, Louisiana, Michigan, Missouri, and Pennsylvania are also considering setting up these accounts. According to Adriann Murawski, NAR’s state and local government affairs representative, NAR and its state counterparts have been actively promoting efforts to have more states provide funding for these accounts.[5]

More relaxed gifting standards within reasonable underwriting guidelines can also make a home purchase more affordable. For example, Fannie Mae allows all the downpayment for one-unit principal residence property mortgages with loan-to-value of greater than 80 percent (or downpayment of 19 percent or less) to come from eligible givers (persons related by blood or marriage, fiancé, fiancée, or domestic partner.[6] Freddie Mac allows gifts/grants after the borrower puts in a three percent downpayment.[7] The Federal Housing Administration allows the 3.5 percent downpayment to come from acceptable donors (relatives, employer, friend, charitable organization, government agency) for borrowers with credit score of at least 620. However, if credit score is between 580 and 619, the downpayment must be the borrower’s own money (required minimum investment). The builder, seller, or an associated entity to the transaction may not provide gifts.[8]

[1]NAR’s 2017 Home Buyers and Sellers Report reported a median downpayment among first-time buyers of five percent in 2017, slightly down from six percent in 2014-2016.

[2] For FHA-insured loans, the upfront mortgage insurance premium (UFMIP), which can be financed as part of the mortgage, is 1.75 percent, and the annual mortgage insurance premium (MIP) is 0.85 percent on 3.5 percent downpayment loans.

[3] This is equivalent to 20 percent of the median home price of $233,800 in 2016. Based on NAR’s 2017 Home Buyers and Sellers Report, the median price of first-time buyers is 80 percent of the median price of all buyers.

[4] Given current low rates on savings, income tax deductibility on interest earned on these accounts is a blunter incentive compared to income tax deductibility based on the contribution (similar to IRA accounts).

[5]Carrns, Ann. How Some States Are Helping First-Time Home Buyers. New York Times. https://www.nytimes.com/2017/12/08/your-money/first-time-home-buyers.html. December 8, 2017.

[6] Fannie Mae. See https://www.fanniemae.com/content/guide/selling/b3/4.3/04.html

[7] Freddie Mac. See http://www.freddiemac.com/homepossible/home_possible_faq.html